Do you own an investment property and are looking to sell it to buy another property? Or are you hoping to pursue other property investment ventures? You may want to consider a 1031 exchange. A 1031 exchange refers to Section 1031 of the United States Internal Revenue Code. Language within that section of the law presently allows taxpayers to defer recognition of capital gains and federal income tax liability on certain types of properties.

Current 1031 exchanges originated in the Revenue Act of 1921. This act introduced tax deferral for non like-kind property and security exchanges by investors. Minor modifications were made in 1924 and 1928. In 1935, the Board of Tax Appeals approved tax deferral for like-kind exchanges, which eliminates capital gains tax liability for the exchange of similar assets. The 1935 amendment also added in qualified intermediary language and retained the “cash in lieu of” clause.

Continue reading and this article will delineate the usage of 1031 exchanges, and unpack the advantages available to real estate investors through this portion of the tax code.

Covered in this article:

- What is a 1031 Exchange?

- Why Investors Seek Out 1031 Exchanges

- Types of 1031 Exchanges

- 1031 Exchange Timeline

- 1031 Exchange Timeline Explained

- Commercial Real Estate Like-Kind Exchanges

- 1031 Exchanges for Real Estate Investors

Why Investors Seek Out 1031 Exchanges

Real estate investors use 1031 exchanges for many reasons, the foremost being the ability to defer 100% of capital gains and other taxes. This reduces tax liabilities, freeing up capital for the acquisition of additional investment properties.

If real estate investors do an exchange into a commercial real estate (CRE) fund such as a Delaware Statutory Trust (DST) property, here are the key benefits:

- Increased cash flow and purchasing power

- Decreased amount of income taxes, achieved through depreciation

- Accelerated diversification of an investment portfolio, and better capacity to take advantage of growing industries

1031s present a unique opportunity for investors. Demand increased throughout 2021, with the syndicated 1031/DST market raising a record-breaking $7.4 billion in equity. Of course, there is inherent risk in any investment, and the risks of 1031 exchange DST include the fact that there are no guarantees for projected appreciation, interest rates can change, illiquidity can occur, and more. However, when balancing risks against opportunities, investors are willing to engage in this sector, many with great success.

Types of 1031 Exchanges

There are four types of 1031 exchanges:

1. Simultaneous exchange — When relinquished and replacement properties close on the same day, it may fit the criteria for a simultaneous exchange. A qualified intermediary is required to handle the exchange.

2. Delayed exchange — Commonly used by investors, the delayed 1031 exchange happens after a sale and purchase agreement. A third-party intermediary then initiates sale of the property, holding proceeds from that sale in trust for 180 days. Investors have 180 days to complete the sale of a like-kind property.

3. Reverse exchange — Reverse exchanges most often require all cash in a “buy first, exchange later” transaction between two parties. It is subject to a 180 day close window to complete sale of a replacement property.

4. Construction or improvement — In a construction or improvement exchange, a property owner may defer gain on a sold property, held by a qualified intermediary, for 180 days. In that time, exchange equity must be spent on construction or property improvements, or be used as a down payment by day 180.

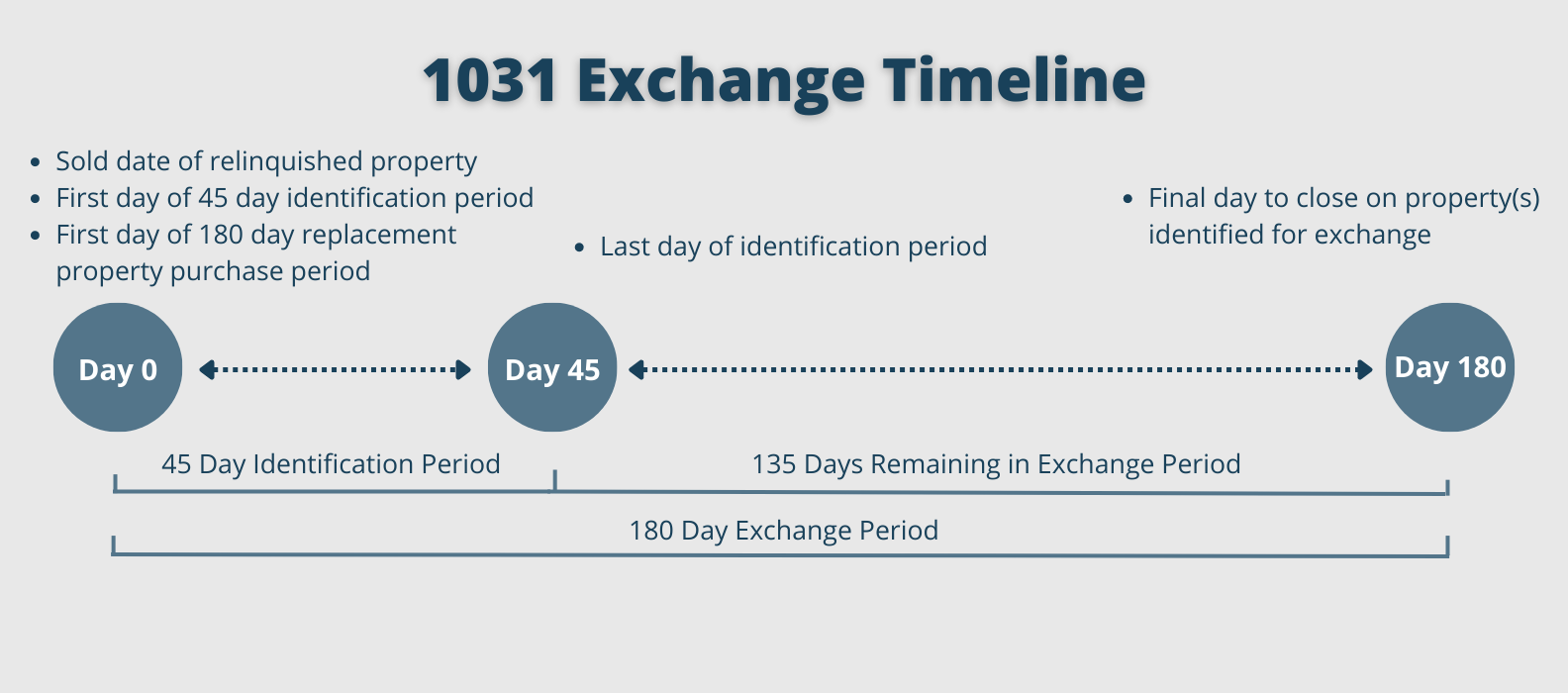

1031 Exchange Timeline

All 1031 exchanges are filed through the IRS, and subject to a 1031 exchange timeline. The two deadlines that govern any 1031 exchange are the identification of a replacement property in writing within 45 days and acquisition of a new property within 180 days. If the exchange is not completed within the taxpayer’s tax deadline, they may be able to file an extension to align with the 180 day exchange period.

There are seven steps to any type of 1031 exchange:

Step 1: Identify the property you want to sell.

Step 2: Identify the property or properties you want to buy, keeping in mind that a like-kind exchange will require additional adherence to specific rules.

See more details below on the qualifications for a like-kind exchange.

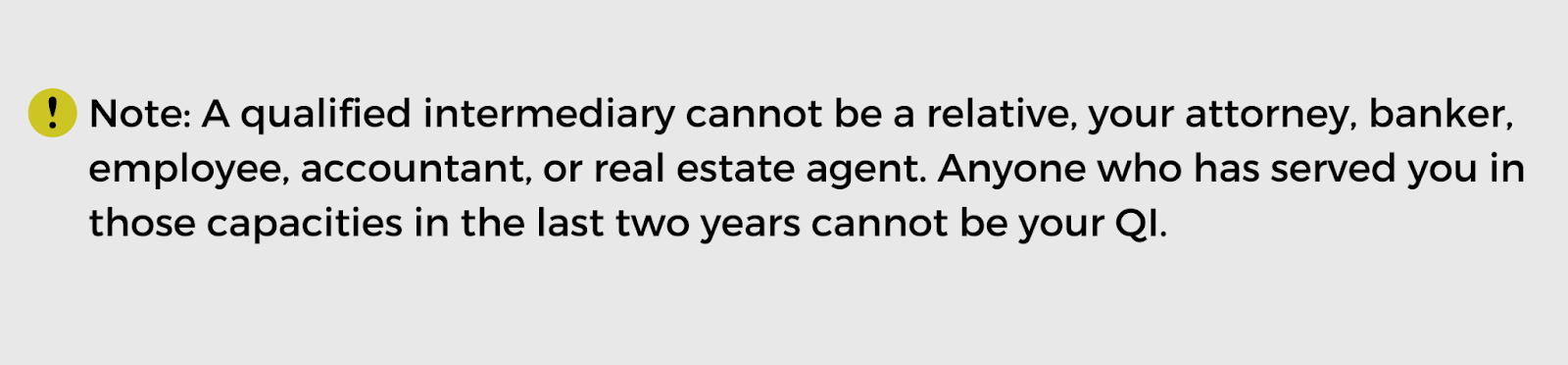

Step 3: Choose a qualified intermediary (QI).

Step 4: Decide how much of the sale proceeds will go toward the new property or properties.

Step 5: Plan your time accordingly.

Step 6: Report your transaction to the IRS.

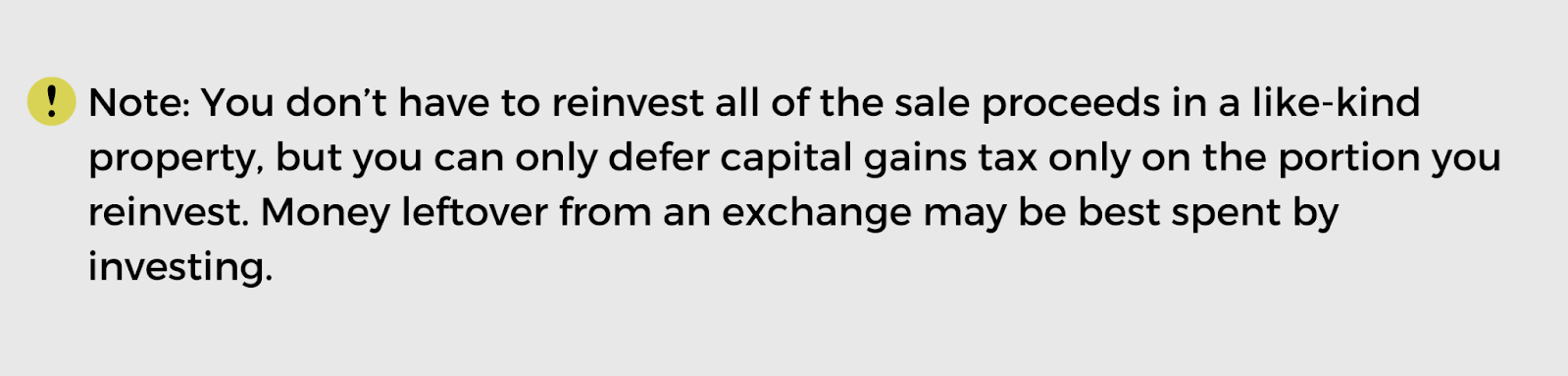

Step 7: Utilize any remaining cash from your sale to avoid paying capital gains taxes.

1031 Exchange Timeline Explained

There are several rules and guidelines to 1031 exchanges. First, the two components related to the 1031 exchange timeline:

- 45-day identification period — Taxpayers have 45 days from the date of sale to identify a potential replacement property. This is known as the 45-day identification period.

- 180-day rule — Taxpayers must acquire a replacement property within 180 days of the sale of the relinquished property.

There is also a time consideration for reverse exchanges:

- Time windows for reverse exchanges — Under the Rev. Proc. 2000-37, if an Exchange Accommodation Titleholder (EAT) begins an exchange, the exchanger must identify (in writing) the EAT’s acquisition of the parked property within 45 days.

A few other rules that dictate how 1031 exchanges may take place:

- The three property rule — According to 1031 exchanges, up to three properties may be identified.

If you have more than three properties you wish to be identified, you may take advantage of the 200% or 95% rule.

- The 200% rule — Under the 200% rule, investors may identify an unlimited number of replacement properties as long as the cumulative value of those properties isn’t 200% more than the value of the sold property.

- The 95% exception rule — A caveat to the 200% rule, the 95% rule gives investors the ability to acquire more than three properties where the total value is more than 200% as long as that individual acquires at least 95% of the value of the identified properties.

- The depreciation recapture rule — A final rule to consider, the depreciation recapture rule. When a property is sold, many investors will have depreciated the property by deducting the cost of wear and usage it received during ownership. Keep in mind the IRS will want to recapture some of those deductions and add them into the total taxable income from the sale. Utilize a 1031 properly, and you can roll the sold property cost basis into the new property.

Commercial Real Estate Like-Kind Exchanges

There are various types of like-kind exchanges which may benefit commercial real estate investors. The rules that dictate what qualifies as a like-kind exchange are as follows:

- It cannot be a taxpayer’s primary residence (see Section 121 of the tax code for a relevant exclusion)

- Both properties must be within the United States to qualify for a 1031 like-kind exchange

- If money, or a non-qualified property, are included, it may result in gain recognition

- Partnership interests do not qualify as a replacement property for relinquished land

- Replacement and relinquished properties must be held by the same taxpayer as a continuation of ownership

Here are the types of commercial real estate like-kind exchanges:

DST 1031 Exchange

A Delaware Statutory Trust or DST 1031 exchange is a great solution for investors who wish to safeguard against market volatility. This type of exchange allows property owners to input funds from a 1031 exchange into a pooled investment that allows them to invest in an asset larger than the property that they are selling and/or a pool of properties to diversify their investment portfolio. This means investors can exchange income from a single property sale for a share of a portfolio of passive real estate investments.

Tenants in Common 1031 Exchange

Tenants in common (TIC) is a form of real estate asset ownership in which ownership is shared between multiple parties, each of whom have a fractional interest in the asset. Tenants in common investments are seen as direct ownership, which means they are eligible for 1031 exchanges. However, TIC exchanges are far less common today than DST exchanges.

1031 Exchanges for Real Estate Investors

1031 exchanges are a powerful tool for real estate investors looking to reduce tax liability, free up capital, and build wealth. It is essential that any investor works with a registered professional to ensure all steps and timelines are met.

The team at Hartman is dedicated to providing insights on the many types of opportunities available to real estate investors. For more information, visit our resources page.

Disclaimer: The information provided above is for general informational purposes only. It should not be considered a recommendation or personalized professional, legal, tax, or advisory advice. Its accuracy or completeness cannot be guaranteed and may change due to changes in regulations, legal, or economic conditions. Please consult with your legal or tax advisor on your individual tax situation.

All investments involve risk including the possible loss of principal. You should familiarize yourself with all risks associated with any investment product before investing.